The ABCs of 12D Chess For 13Fs

“13Fs are like bikinis. What they reveal is suggestive, but what they conceal is vital.”

-Mojo

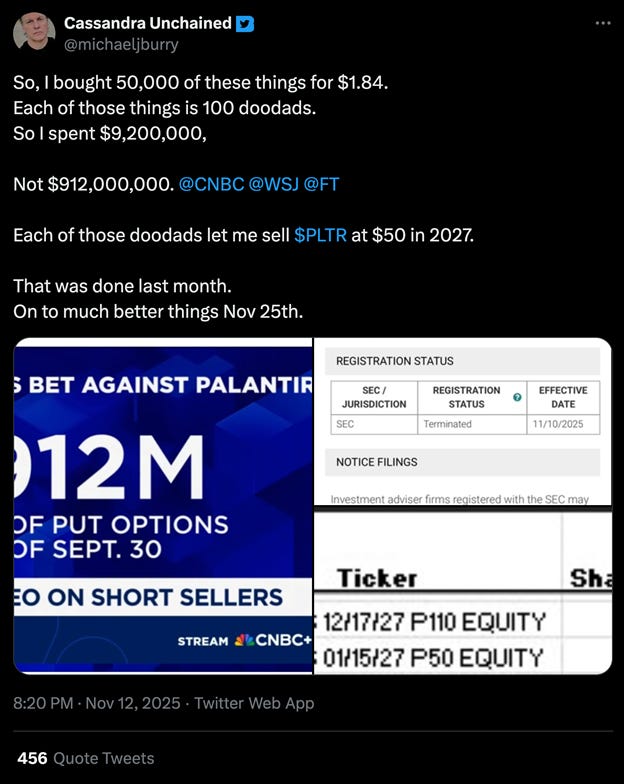

As new 13F filings hit this week, market observers will do what they always do: scrape the names, rank the biggest adds and cuts, and declare who’s bullish or bearish on what stocks. The recent confusion around Michael Burry’s options disclosure offers a useful reminder of how easily even basic filing mechanics can be misread. If the straightforward math of how options appear in mandatory disclosures trips up professional observers, the far more sophisticated positioning strategies that elite funds actually employ remain almost entirely opaque.

For some funds, the resulting market chatter is simply an unavoidable consequence of mandatory disclosure. For others, the attention is welcome, even useful. A few sophisticated firms understand that their 13F itself can move stocks and strategically exploit that reflexivity. Yet regardless of a fund’s sophistication level or how it responds to the attention, what appears in the filing remains the same: a quarterly snapshot of long equity positions that captures only one dimension of a complex, multidimensional portfolio.

A 13F captures only what the SEC requires: primarily long positions in U.S.-listed equities and equity options. It excludes shorts and many other exposures, including credit, swaps, futures, other derivatives, and funding legs and structures that support them. That means when you read a manager’s 13F, you’re seeing a subset of a subset. First, you’re limited to their equity portfolio, which excludes their credit book, macro trades, and everything else. Then, within that equity portfolio, you’re seeing only the long side—no shorts, no hedges, no offsetting positions. It’s technically accurate but functionally misleading.

The raw list of holdings may seem revelatory to the uninitiated, but it frequently does not capture even a fraction of the true economic exposure at stake. What appears as a bullish stake might be fully hedged or boxed. What looks like a conviction long could be a merger arb leg or a volatility trade in disguise. The form shows you what a fund owns, but it rarely tells you why they own it, how it fits into the broader strategy, or what they’re actually betting on.

Consider Elliott Investment Management’s approach. Their 13F shows large equity holdings — industrials, energy, technology — and a web of index and sector puts. On paper, it looks like a bullish, diversified book. In practice, it’s a neutralized event engine. Elliott doesn’t primarily buy stocks because they like the business; they buy them as carriers for a specific catalyst, often one they intend to create themselves. Their real exposure is to the idiosyncratic path that their own pressure sets in motion — the market’s repricing of a company once they step in.

The principle extends beyond activism—multi-strategy funds, macro traders, and equity long/short managers each layer complexity differently—but activist campaigns make the clearest case study.

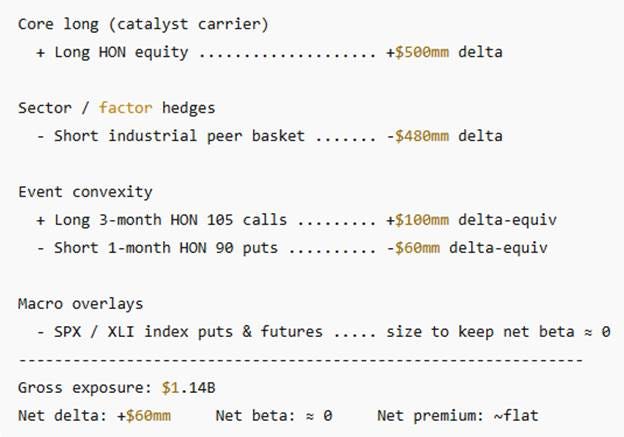

Before they go public with a campaign, activists have already built their position block. They’re long the target stock, short a basket of correlated peers, and running overlay hedges against the sector and the market (see Scooby Doo & The Case Of The Mysterious Oracle CDS). The math typically nets out near flat delta and zero beta. The options book adds convexity: long calls, short puts, sometimes call spreads around the expected event window. That structure isolates one thing only: the company-specific spread their activism creates. When the catalyst hits and the stock moves, they monetize the convexity, re-hedge the deltas, and lock in gains. The goal isn’t so much to own Honeywell or Phillips 66 as it is to own the repricing of Honeywell or Phillips 66 created by their own footprints in the market.

Position Block

Behavior snapshot

· Market drifts up 2%: both HON and the basket rise — near-flat P&L in core position block (short puts long calls generate small profit).

· Catalyst hits (+10% HON idiosyncratic move): stock outperforms, calls expand, short puts decay — ≈ gain.

· Post-event: hedges added, short puts covered or expire, calls sold or rolled into spreads, beta re-centered.

This is what a real activist position block typically looks like. The long equity line is just the anchor leg. Wrapped around it are short baskets, derivatives, and funding trades that sterilize everything the fund doesn’t want — market exposure, factor drift, unwanted beta. What remains is pure idiosyncratic alpha: the mispricing created or accelerated by the fund’s own intervention. Once that alpha is isolated, it’s levered through prime brokers.

The smaller, scattered positions inside a 13F often tell you more about the hidden book than the big ones do. Those odd lots are usually hedges, borrow boxes, or partial pairs that keep net exposure damped down. The options and swaps that don’t show up complete the picture: short puts against shorts, short calls against longs, cross-hedges in related names, synthetic shorts where borrow is tight.

Once you read a 13F through that lens, the illusion that you’re seeing the manager’s revealed investment opinions dissipates. Elliott’s portfolio isn’t primarily a set of directional bets on companies; it’s a matrix of catalysts, spreads, and hedges. The fund is long what it can influence, short what it can’t influence to neutralize “gotcha risk” (see Scooby Doo & The Case Of The Mysterious Oracle CDS), and levered where the path is asymmetric.

Elliott isn’t necessarily betting that Honeywell is undervalued—they’re betting on the reflexivity embedded in Elliot’s own public campaign around Honeywell. Their Honeywell position isn’t primarily directional; it’s reflexive. The fund builds positions in what it can reflexively influence, hedges out what it can’t control, and levers the spread between current reality and the future they’re actively constructing. The conviction isn’t in owning the company; it’s in being in control of the reflexivity around the company. Elliot likely extracted their required return within days of announcing the campaign. Any future operational improvements or business re-ratings after that point are free lottery tickets that they are holding.

This is the real anatomy of sophisticated capital deployment by modern hedge funds, and it’s the reason that treating 13F filings like stock-picking scorecards misses the entire game. These documents are quarterly freeze-frames of multidimensional systems in constant motion—static images of pawns being deployed in a sophisticated game of 12D chess. The real edge is less about the specific names on the list; it’s in the architecture around them, the catalysts embedded within them, and the asymmetries extracted from them. When observers debate whether a fund is bullish or bearish based on a 13F, they’re analyzing a chessboard where only the pawns are visible. The filing shows you a few pieces, but the bishops, rooks, and queen—the shorts, the hedges, the derivatives—remain completely hidden unless you have experience executing similar strategies yourself.

If this piece meant something to you, share it with someone who could benefit.

I’ll be writing more on governance, activism, dark arts trades, and investment process. I’ve also written about tokenization, Formula One, the NBA, and sometimes just tell a story worth remembering. Stay tuned.

You can also find me on Twitter at @MrMojoRisinX and @BeWaterltd.

Hi Mojo

Thank you so much for your write-up. An insightful piece from people from outside the hedge fund insdustry. Particularly, I am coming from the Private Equity industry, although I am looking for learning more about Hedge Fund strategies as the Position Block you´ve mentioned on your write up. Any recommendations to learn more about this kind of structures? Thank you