CEF Activism at an Inflection Point

What BlackRock Doesn't Want You to Know About CEF Activism

My favorite opportunities come from what I call, "doorjacks," which are violent security (equity and / or credit) dislocations that happen when low probability events that few investors positioned for actually materialize.

But, sometimes you stumble onto something bigger than a trade. The Supreme Court just agreed to hear a case that could significantly reshape how activists challenge corporate governance across America. The case centers on closed end fund activism, a corner so obscure that even sophisticated investors barely understand it. But the legal precedent being set could ripple far beyond sleepy municipal bond funds.

If the justices rule the wrong way, they might gut one of the primary weapons activists use to challenge entrenched management. This isn't just about investment strategy. It's about whether change agents can maintain meaningful leverage in boardrooms, or whether defensive management teams get judicial blessing to make shareholder pressure less effective.

Understanding the Legal Framework Under Attack

Saba Capital, the hedge fund run by Boaz Weinstein, sued a series of closed end funds under Section 47(b) of the 1940 Investment Company Act for adopting defensive measures designed to dilute activist voting power. The Second Circuit ruled in Saba's favor, but now the Supreme Court will decide whether private investors have the right to bring these lawsuits at all.

Section 47(b) provides that contracts made in violation of the Investment Company Act are generally unenforceable, and courts may grant rescission "at the instance of any party" unless doing so would be inequitable. That phrase "at the instance of any party" is the crux. Does it create an implied private right of action allowing shareholders to sue, or does enforcement belong exclusively to the SEC?

The circuit courts split on this question. The Second Circuit ruled that the language "necessarily presupposes that a party may seek rescission in court by filing suit" and is "effectively equivalent to providing an express cause of action." But the Third and Ninth Circuits reached the opposite conclusion.

This isn't legal semantics. Private litigation creates leverage that pure regulatory enforcement cannot match. When activists can threaten direct lawsuits for governance violations, boards take shareholder concerns (more) seriously. Remove that threat, and you're left with proxy fights and shareholder proposals, tools that entrenched management can more easily ignore.

The government sided with the funds, filing an amicus brief arguing that private lawsuits could have "unpredictable impacts" on the fund industry. Industry groups like the U.S. Chamber of Commerce piled on, claiming private litigation would open "floodgates" of disruptive cases.

Translation: shareholders should have fewer tools to challenge management and board decisions.

Why Closed End Funds Are the Perfect Laboratory

CEFs have a beautifully simple value proposition: they trade at market prices but hold portfolios marked to net asset value daily. When market price trades below NAV, that's mathematical inefficiency activists can target with surgical precision. No need to analyze competitive positioning or management quality. You're betting a 15% discount to NAV will close because arithmetic says it should.

This mathematical clarity makes CEF activism the purest form of shareholder advocacy. Activists aren't trying to improve operations or change strategy. They're forcing boards to address structural discounts that exist purely because management isn't serving shareholder interests effectively.

That precision is why CEF activism became so effective, and why it's under legal attack. When activists can systematically identify mathematical inefficiencies and use multiple pressure points to force correction, they've created a machine for extracting value from management negligence. Boards hate that predictability.

But what's happening now is unprecedented in scale and sophistication. CEF activism has existed for decades. Phillip Goldstein and others have been running campaigns since the 1990s, typically targeting one or two funds at a time with limited resources. What makes Boaz Weinstein's Saba Capital different is the systematic approach: attacking the entire CEF ecosystem simultaneously across dozens of funds, using multiple legal strategies, coordinating timing across campaigns. It's a full frontal assault by air, land and sea that the CEF space has never seen before.

This systematic approach is what has boards and asset managers so concerned. Individual activist campaigns were manageable. A coordinated assault on the entire structural inefficiency of the CEF market threatens the business model itself.

RIV: The Reconnaissance Tool

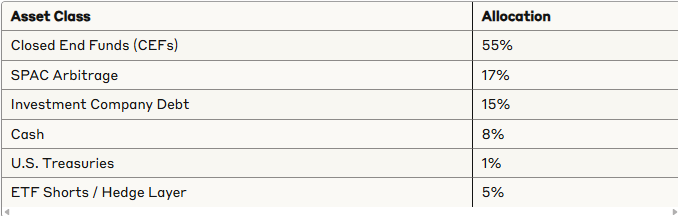

RiverNorth Opportunities Fund (RIV) is a closed end fund that buys other closed end funds. At first glance, it's just a meta fund collecting a ~12.75% distribution while waiting for discounts to normalize. But RIV is a real time window into the most sophisticated activist operation in the CEF space.

RIV buys closed end funds trading at discounts, using 33% leverage to amplify returns when discounts compress. Most of the time, that means collecting yield and waiting for mean reversion. But during market stress, when discounts blow out and panic selling intensifies, RIV becomes a weapon designed to profit from chaos.

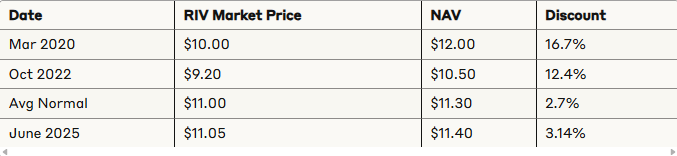

During March 2020, you could buy RIV for $10 when its holdings were worth over $12. Not because portfolios were worthless, but because the entire CEF pricing mechanism had broken down. RIV stepped in to buy the carnage, creating "discount squared"; a discounted fund buying other discounted funds.

RiverNorth isn't running a passive strategy. They're actively hunting mispricings across multiple strategies. More importantly, their CEF selections often overlap with holdings of major activist shops like Saba Capital, Bulldog Investors, and Karpus Investment Management.

That overlap isn't coincidence. It's coordination without coordination, revealing where multiple sophisticated players see the same opportunity. Track that overlap in real time, and you get early warning signals for the next major activist campaign.

Gang Theory: Coordination Without SEC Violations

The same names keep showing up in different portfolios for reasons that go deeper than coincidence. But activists must be careful about coordination, because SEC rules around group formation create significant legal constraints.

Under Section 13(d), any person or group acquiring beneficial ownership of more than 5% must file public disclosure within 10 days. If multiple investors "act as a group" for acquiring, holding, or voting securities, their combined holdings count toward that threshold.

The definition of "group" is where things get complicated. A group exists when two or more persons agree to act together for securities purposes. But what constitutes "acting together"? Sharing research? Discussing strategy? Coordinating timing?

CEF activists have developed sophisticated approaches. They avoid explicit coordination that would trigger group filing requirements. Instead, you see patterns suggesting implicit alignment. When RiverNorth, Saba, Bulldog, and Karpus all show up in the same CEF, it's because they're running similar analytical frameworks identifying the same mathematical inefficiencies.

The 13D filings start landing. Proxy advisors take notice. Media picks up the story. Suddenly, a sleepy municipal bond wrapper becomes ground zero for a governance campaign. The pressure builds systematically without explicit coordination.

Take the 2023 Bulldog campaign against MFS High Yield Municipal Trust (CMU). Bulldog's 13D filing was the spark. CMU announced a tender offer soon after. RiverNorth had quietly filed its own 13G before the tender offer's execution. They didn't need to initiate the campaign. They rode the pricing wave and exited before volatility dried up.

The CMU trade delivered 15%+ returns in months. Not because municipal bonds rallied, but because Bulldog forced a tender offer that closed the mathematical discount. Pure arbitrage masquerading as activism.

Why CEF Activism Succeeds Where Traditional Activism Often Fails

Traditional shareholder activism faces enormous structural obstacles that make success less predictable and expensive. Staggered board elections mean replacing directors takes years. HG Vora's ongoing campaign against PENN National Gaming illustrates this challenge. Despite winning board seats, HG Vora must wait another election cycle to gain meaningful control over governance changes. With activists now on the board, PENN's management likely recognizes the inevitable and may quietly evaluate strategic alternatives including a company sale. The campaign could be just beginning rather than concluded, but the timeline uncertainty exemplifies why traditional activism requires patience and deep pockets and introduces many other variables that can result in investor losses.

CEO employment contracts create additional hurdles. Terminating underperforming executives often triggers golden parachutes worth tens of millions. Founders with special voting rights can ignore shareholder pressure entirely. Poison pills and defensive measures can be adopted quickly to frustrate activist campaigns.

Proxy advisory firms wield enormous influence over institutional voting, but swaying them requires sophisticated campaigns that blend legitimate governance concerns with political messaging. The process is as much art as science, and arguably susceptible to influence that goes beyond pure merit.

CEF activism strips away much of this complexity. Reading fund bylaws matters more than analyzing competitive positioning. Understanding voting thresholds trumps modeling cash flows. You're not trying to improve a business. You're forcing math to work correctly.

The timeline clarity makes all the difference. CEF activists can force specific votes on specific dates with specific outcomes. Either the tender offer passes or it doesn't. Binary outcomes with defined catalysts.

That predictability is exactly what makes the Supreme Court case so significant. When activists can systematically identify mathematical inefficiencies and use legal leverage to force correction, they've created a repeatable process. If that legal leverage gets weakened, the entire framework becomes less effective.

The BlackRock Factor: When the House Always Wins

The elephant in the room is BlackRock and Larry Fink's asset gathering machine. BlackRock fights dirty when threatened, then pivots aggressively when momentum shifts. They opposed Bitcoin and crypto until it gained unstoppable momentum, then launched the largest Bitcoin ETF in the world. Pattern recognition suggests similar behavior in the CEF space.

BlackRock's recent battle with Saba Capital illustrates their defensive playbook perfectly. When Saba targeted ten BlackRock CEFs worth $10 billion, BlackRock deployed sophisticated shareholder communications, leveraged defensive bylaw provisions, and won the initial proxy battles. Only 11% of shareholders voted for Saba's proposals despite compelling mathematical arguments about persistent discounts.

But the story reveals BlackRock's deeper strategic thinking. Rather than declaring victory and moving on, BlackRock negotiated a settlement seven months later that provided exactly what Saba had been demanding: massive share buybacks at near NAV prices. BlackRock agreed to buy back 50% of outstanding shares in its BlackRock Innovation and Growth Term Trust and 40% of outstanding shares in Health Sciences Term Trust for 99.5% of each fund's net asset value, totaling roughly $1.6 billion.

In return, Saba agreed to stop its campaigns at dozens of BlackRock funds calling for fresh directors to be installed and for BlackRock to be fired as some of the funds' manager. BlackRock effectively bought peace by giving Saba a massive payday while extracting a standstill agreement that neutralizes their most persistent critic.

This reveals BlackRock's ultimate game. They fought the proxy battles not to win permanently, but to control the timing and terms of any settlement. By forcing Saba to spend months on campaigns before agreeing to buybacks, BlackRock demonstrated that activism is expensive and time consuming even when ultimately successful.

This reveals BlackRock's deeper game. If CEF activism gets neutered by the Supreme Court ruling, those assets don't disappear. They flow into BlackRock's ETF ecosystem where investors get worse disclosure, more overlap, and less control. Shareholders who had mathematical recourse through CEF activism get stuffed into ETFs with identical underlying holdings but no ability to force discounts to close.

BlackRock wins regardless. Fewer activist threats in the CEF space means higher fees and less pressure. If activism kills the CEF structure entirely, those assets migrate to ETFs where BlackRock dominates market share. The ultimate asset gathering machine benefits from either outcome while retail investors lose leverage.

During market crashes, this becomes especially problematic. CEF investors can at least see their discounts widen and bet on mean reversion. ETF investors holding the same underlying assets through BlackRock products get no such transparency or opportunity. They discover their exposures during market stress, not before.

The Activist Resistance Playbook

Even perfect math doesn't guarantee victory. Successful activists like Saba have faced sophisticated defensive tactics that show how boards resist shareholder pressure.

Bylaw amendments provide powerful defensive tools. Boards can raise thresholds for shareholder proposals right before campaigns heat up. Suddenly, you need 25% ownership to call a special meeting instead of 10%.

Saba's experience with Voya illustrates these tactics. Despite accumulating 24% ownership, Saba lost when the board changed voting requirements days before the election. Instead of needing a majority of votes cast, they needed 60% of all outstanding shares. Only 56% of shareholders participated, making victory mathematically impossible regardless of vote tallies.

But Saba's track record shows initial setbacks don't mean permanent defeat. Their BlackRock campaign "failed" in proxy votes but led to $1.6 billion in buybacks. Persistence often forces some form of shareholder friendly outcome because the mathematical inefficiency doesn't disappear after a proxy vote. (link to comment letter: https://www.sec.gov/comments/s7-24-16/s72416-9006543-246026.pdf)

Some boards choose the nuclear option: liquidation on their terms. They announce managed wind downs, distribute assets over months, and claim they're maximizing value. The discount disappears because the fund disappears. Activists get NAV realization, but the process drags out and fees eat returns.

The key insight is that activist "failures" often produce partial victories or eventual settlements. Mathematical inefficiencies create persistent pressure that doesn't vanish because activists lose a particular vote.

The Death Spiral Scenario

If private litigation disappears entirely, CEF discounts might become systematically permanent, creating a death spiral that makes the entire structure obsolete.

Without activist litigation threats, boards have less reason to address persistent discounts. Shareholders can't force tender offers through legal action. Proxy fights become toothless when boards can ignore results. The mathematical inefficiency that attracts capital becomes unfixable.

Discounts widen because there's no compression mechanism. Investors stop buying CEFs because structural inefficiency never resolves. Fund managers see assets shrink, meaning lower fees. They shut down funds or stop launching new ones. The sector withers.

This creates a paradox for RIV. In a world where CEF discounts stay persistently wide with no activist pressure, RIV might become the only viable way to capture that value. They'd be the last buyer standing in an abandoned market.

But there's another scenario. Even without activist litigation, pure macro dislocations could create larger opportunities than activism ever provided. During market chaos, when underlying holdings blow out to 15%+ discounts and RIV trades at 15% discount, you're getting 15-18% yield while sitting on massive discount compression potential at two levels.

The mathematics become compelling even without activist catalysts. Short term returns during macro stress might be higher, even if frequency decreases. Activism provided predictability and timing (and is a seasonal trading playbook I utilize via systematic sourcing / origination and trade structure process; HINT: I may write about this in the future…). Pure dislocation plays could generate bigger gross returns because setups are more extreme.

Using RIV as Early Warning System

Smart money uses RIV's portfolio, cross referenced with Saba's holdings and Bulldog's 13Ds, as a real time map of where activist campaigns might build.

Pull RIV's quarterly holdings. Cross reference with BRW (Saba's CEF fund). Look for names where multiple activists accumulate shares. When the same CEF names show up across activist portfolios, investigate.

Check discount to NAV, review fund bylaws, examine board composition. For example, NUV (Nuveen Municipal Value Fund) currently trades at 11% discount and shows up across multiple activist holdings. GLO (Clough Global Opportunities Fund) sits at 13% discount with similar overlap patterns.

Signal recognition is key: persistent discounts above 10%, boards that haven't addressed shareholder concerns, upcoming elections. Municipal bond CEFs tend to be fertile ground because they have retail heavy shareholder bases and sleepy boards.

You don't need to buy RIV to play individual opportunities. Buy specific CEFs directly, size positions for event driven situations, capture full discount compression when campaigns launch. The reconnaissance shows you where to look before campaigns become obvious.

But there's another advantage to the RIV approach: disclosure thresholds. While activists like Saba must file 13D forms once they hit 5% ownership and signal their intentions publicly, RIV and other opportunistic players can operate below 4.99% with no disclosure requirements. They get a "free look" at activist situations without telegraphing their positions or triggering defensive responses from boards. It's reconnaissance with plausible deniability.

The framework also works for pure macro timing. When CEF spreads start widening, it often signals liquidity pulling back, credit stress building, or forced selling intensifying. Those patterns frequently lead broader market dislocations because CEF structure is more sensitive to liquidity withdrawal.

Three Approaches for Different Mandates

For RIAs and Wealth Managers: During macro dislocations, scale into RIV when spreads blow out. You get professional management and structural alpha without becoming an expert in proxy fights. When VIX spikes above 40 and CEF discounts widen, RIV captures dislocation without individual name work.

For Stock Pickers and Hedge Funds: Use RIV as reconnaissance, then go deep on individual names. Track overlap data, read proxy statements, understand board dynamics, play specific campaigns for maximum alpha and issue spot. Potentially capture 15%+ returns in months by betting on defined event paths.

For Macro Observers: Use CEF spreads as early warning for broader market stress. When discounts widen across the complex, it signals deteriorating liquidity before stress shows up in widely watched indicators. Use that information to prepare portfolios, add hedges, make opportunistic moves.

March 2020: When the System Worked

The framework proved itself during the COVID crash when system wide CEF discounts exploded. Municipal bond funds gapped down 15%, equity CEFs cratered 20%, even Treasury funds traded below NAV.

Overlapping across activist portfolios and tactical funds like RIV were names that would later become takeover targets and activist victories. The sophisticated money was accumulating while markets felt chaotic, preparing for inevitable mean reversion.

RIV didn't lead activist campaigns. It bought mispricing, spreads / discounts widen, and waited for Saba, Bulldog, or others to apply pressure. Multiple players converging on the same mathematical inefficiencies, using diverse pressure points to force correction.

It worked because activists had tools. Remove those tools, and the system becomes less efficient at correcting mathematical inefficiencies.

What Comes Next

The Supreme Court case will be decided during the next term. If the justices significantly limit private litigation rights, CEF discounts could become more persistent as boards face less pressure. Traditional corporate boards might become more willing to adopt defensive measures if activist litigation threats diminish.

But we could see adaptations. Activists might develop strategies that don't rely on federal securities litigation. State law remedies could become more important. Institutional investors could become more active in governance decisions.

The macro dislocation opportunities don't disappear regardless of legal developments. During market stress, CEF discounts will blow out as liquidity disappears. The leverage and mean reversion dynamics that make RIV attractive during chaos don't depend on activist litigation.

What might change is how systematically inefficiencies get corrected, how predictably pressure builds on underperforming boards, and how effectively shareholders can force mathematical discrepancies to resolve.

Whether the Supreme Court case represents minor adjustment or significant shift depends partly on how broadly the justices rule and partly on how markets adapt. What's clear is that we're documenting how a sophisticated system for identifying and correcting mathematical inefficiencies works while that system is potentially under legal challenge.

The mathematical inefficiencies that make CEF activism possible aren't disappearing. Closed end funds will still trade at discounts during market stress. Leverage will still amplify returns when discounts compress. Mean reversion will still create opportunities for patient capital.

What might change is how systematically those inefficiencies get corrected, and whether investors who understand current mechanics will be better positioned to adapt to whatever framework emerges from this legal and market evolution.

You can also find me on twitter at @MrMojoRisinX.