The Factory That Makes Investment Processes Repeatable

At 2:47 AM on a Tuesday in early March 2009, I was hunched over merger documents in an empty office, trying to figure out whether Dow Chemical could actually close its $15.3 billion acquisition of Rohm & Haas. Credit markets had frozen, and the deal needed additional alternative financing. The original timeline meant nothing. That period solidified for me the wisdom that when everything breaks down, systematic process becomes your lifeline. The mapping I'd done ahead of time, tracking every financing amendment and pressure point, became the only reliable guide through the chaos.

Around these parts we talk about process:

https://mojo3324106.substack.com/p/everyone-has-a-process

The most repeatable investment frameworks emerge from the most constrained environments. This is why merger arbitrage creates some of the best investors’ processes. The constraints make you better. Merger arbitrage forces systematic thinking and mastery of process in ways that picking growth stocks never could. You have a finite set of tools (read the agreement, map the timeline, assess regulatory risk, size appropriately), but the binary nature of outcomes and defined timelines force you to master each element systematically rather than relying on market momentum or storytelling to cover for sloppy process.

It doesn't make news headlines on Bloomberg very often anymore, unless a fund blows up or makes a big bet on a volatile deal spread that closes against what seemed like difficult odds. It doesn't provide the narrative adrenaline rush, nor does it generate the unlevered returns of compounders or directional bets. However, merger arb is repetitive, systematic, has a high Sharpe ratio and—if you do it well (and potentially utilize leverage opportunistically)—quietly profitable. That's exactly why it's the ideal place to start talking about investment frameworks.

I've run this process through multiple market cycles now. Long/short across the capital structure, event-driven space and merger arbitrage. I was once the most junior analyst on the desk that sat closer to the printer than my boss—I was the guy tearing through merger docs at all hours in a small conference room with takeout food everywhere.

I became a PM sizing positions through the Global Financial Crisis. I have run risk oversight watching the same systematic process get executed across multiple strategies, including sector based long/short, event, merger arb, appraisals, and activism.

What I learned is this: from the outside, merger arb can look pretty boring, and at times very stressful and hectic with otherwise symmetric payoffs. You have to get up to speed very quickly on the announcement day. But most deals are orderly. Vanilla holders sell to the arbs, there's usually a trading hiccup mid-morning where you want to set your spread to get some position on while you tighten up the event path assessment, then you wait for the real disruptions—HSR second requests, vote issues, regulatory challenges to increase your position size.

Before we jump in with both feet into framework; here's something that often gets under looked across multiple strategies and that's your fund terms: your fund terms customize everything within the same basic framework. A book with monthly liquidity can't really size names and manage risk the same way as one with two-year locks—it needs different rules, different construction approaches. They are not entirely different processes, but rather intelligent customization inside the same systematic thinking.

Why The Merger Arb Laboratory Matters

Many of the most well-known hedge funds and even proprietary trading desks were built on merger arb. Before long/short equity ruled the pod model, this occurred because the foundation scaled inside risk systems. Merger arbitrage strips investing down to its essential elements. You have clear catalysts, defined timelines, and measurable probabilities. Feedback loops that kept you honest. When cycles flipped, the same process thinking carried firms into distressed credit, restructurings, and eventually into shareholder activism.

Today, catalysts are softer/fuzzier and durations longer and less defined, which only makes discipline more valuable. Merger arb remains the purest laboratory for building systematic thinking. The principles apply everywhere: define your universe, filter it, rank it, diligence it, size it, construct around it, manage the risk. Then cycle through again.

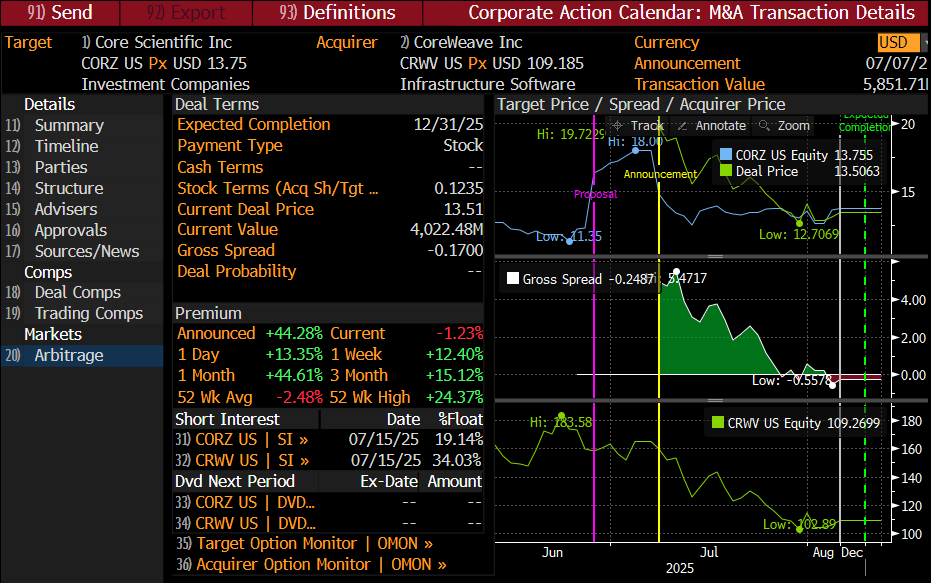

About 95% of announced deals closed successfully from 2010-2021, spanning the post-crisis recovery and COVID disruption. But that aggregate statistic hides the real opportunities and dislocations that occur in merger arb. Most deals have hiccups where new information surfaces—sometimes leaked intel that's incentive-driven, other times genuine fundamental developments—and spreads widen, probabilities shift, risk-reward looks more attractive but the deal “feels less safe”. The entire chain moves, then often reverts back as more information gets disclosed in filings that need interpretation.

The Universe: Building Your Information Engine

If it's not in your universe, it doesn't exist. Every process starts here: a live feed of every announced deal, updated daily. Price, spread, expected close, break price, structure. You should track names you'll never trade because contagion runs deep—one failed cross-border deal and "safe" domestic names gap down in sympathy.

But logging the deal is just the beginning. You map the entire event path, and this deserves its own focus because it's where pattern recognition from your universe database really pays off. You can use historical data to get exact dates on when filings are supposed to happen, when regulatory timelines typically develop, as well as voting processes and the influence of proxy solicitation firms. Then you connect this back to the merger agreement and proxy statement to build your timeline.

The Filter: Your Immune System

Your filtering process protects you from yourself. Hard exclusions come first: hostile bids, illiquid microcaps, CVR-heavy structures your fund can't hold. These are rules that have to be followed, and some cases eliminate highly attractive opportunities. Soft filters follow: regulatory nightmares, shaky financing, deals where the buyer's track record makes you nervous. Ask yourself, do you transact in LBO deals or just strategic transactions?

Draw these lines early. The worst time to debate philosophy is after a spread gaps and you're staring at a loss. Build your own 'one pager' tear sheet for every deal you are involved in with all pertinent transaction information, how you think about different upside/downside deal scenarios, key event path dates as well as earnings, conferences, etc, and closely tracking your break price.

Some managers build heuristics around sponsor behavior. I knew one PM who sized up every Thoma Bravo deal automatically to max size—called them the cleanest closers in the LBO game because reputation risk mattered to them. Another systematically faded Apollo and Cerberus deals, scarred by prior deal issues and breaks.

Ranking: The Probability Engine

Even after filtering out based on specific exclusions, you'll likely still have a lot of transactions. So you rank them, and ranking is where art meets science. Gross spread matters, but RoR (rate of return) matters too. Deal size and liquidity matter as well. Break-price math matters because markets love humbling assumptions, so it is important to beta value adjust your break price using comparable company analysis and even looking at precedent transactions and understanding the holder base after filings have been updated.

But ranking is context. How much M&A $ volume is live? How concentrated is arb capital? What do merger spreads look like versus credit spreads? When both widen together, you're likely seeing stress creep in the system (https://mojo3324106.substack.com/p/cef-activism-at-an-inflection-point). Differentiating between macro and idiosyncratic entry catalysts into widening arb spreads are unique and exciting. Candidly, sliding chips into a macro dislocation (https://bewaterltd.com/p/navigating-multiflation) is easier .

This is probability weighing in real time. You're constantly re-ranking as new information flows in, as timelines shift, as market conditions evolve. The ranking isn't a snapshot, but rather a living assessment that cycles with everything else.

Diligence: Where Process Gets Real

Big spreads look attractive. Many are traps, and it is better to hang around the hoop and wait for the right entry than to passively participate with a full size position. Read the DMA (Definitive Merger Agreement).

Diligence is about running systematic sweeps and even engaging outside counsel at times: Legal terms—MAC clauses, termination mechanics, reverse break fees. Regulatory paths—FTC, DOJ, CFIUS, foreign authorities. Financing structures—commitment letters, syndication and marketing period risk, flex provisions. Consideration details—cash versus stock versus CVRs, presence of appraisal rights and domination agreement investor participants, etc. In some cases, you need to loop in operations to understand whether your fund due to mandate/terms can hold a security post transaction close.

But diligence goes deeper than boilerplate. Merger arb has its dark arts: tracing conditional language through 200 pages of legal text, mapping who has to do what and when, connecting dots management won't say out loud even if you constantly probe them, and in some cases investor relations just doesn't have the ability to answer, but won't give you access to internal counsel, CFO, or business development. You have to wear a lot of hats, and sometimes be a curious part lawyer, part detective, part business analyst and financial analyst.

And you read the credit documents too (sometimes even IPO offering docs), because that's where chokepoints hide. I've seen deals that looked regulatory-killed but died from willful non-cooperation—one side dragging its feet on filings, "forgetting" to provide information, letting timelines slip until someone sued or settled. The headlines said regulatory risk, but the reality was strategic exit.

This is where decision trees come alive. Before you size any position, you map every failure and hiccup mode and what does the backdrop look like using precedents for when this could come to fruition. What happens if DOJ sues? Does a letter from Elizabeth Warren signal, well—anything at all? What if the buyer's stock collapses in a stock deal and drags down the target's price below the deal value (does an activist show up proposing strategic alternatives)? What if the drop-dead date moves six months? These scenarios become your operating manual when chaos hits.

The event path analysis connects everything together. The point here is not simply to read merger agreements in isolation, but to build a comprehensive timeline that anticipates where pressure points will emerge, when deadlines matter, how regulatory processes typically unfold based on your experience and database of historical patterns.

Sizing: Rules with Conditional Triggers

Most blow-ups aren't bad picks—they're simply the result of bad position sizing just like any other blow up. This is where process earns its keep, and it operates on rules-based principles with conditional triggers.

Start with break-price modeling. Layer in beta adjustments. Add liquidity overlays. Look at short interest data and trend. If you can't exit in three days of stress volume (or within fund limits) without burning 50 basis points, you might be too big. Hard caps matter: per deal, per sector, correlation clusters. Multiple deals (strategic and LBO) in sectors like pharma, semiconductors, rails, and chemicals tend to happen at the same time. This adds a lot of complexity and game theory.

But sizing is merely the first layer. Next comes trade construction, and this varies dramatically based on the deal structure.

Trade Construction: Deal-Specific Engineering

Trade construction depends entirely on what you're working with. Cash deals are straightforward—you buy the target and manage downside re using beta adjusted break price, max risk of loss is 150bps and risk of fraud is 400bps (stock goes to zero). Stock deals require you to short the buyer according to the exchange ratio. CVR deals need careful analysis of whether your fund can even hold the contingent payments.

On longer duration deals—anything that might take nine months or more—I often buy way out-of-the-money puts on the target. These eat into your spread profit but define your downside in dollar terms as a percentage of your capital base. Sometimes I'll buy calls on the buyer and puts on the target to hedge tail scenarios.

In addition, depending on your mandate, you can utilize credit instruments to hedge or express better risk-reward for the deal closing? Some situations have bonds, bank debt, or other instruments that give you different ways to play the same bet.

Portfolio Construction: The Next Layer

After individual trade construction comes portfolio-level construction and I look at this as more of a mosaic, but still rules based. Diversify re have concentration limits by buyer type, geography, deal size. Monitor crowding, perhaps create crowding custom baskets and buy conditional custom knock-in put structures.

This cycles back to everything else—your universe coverage, your filtering criteria, your ranking system. Portfolio construction isn't separate from the other phases; it's informed by all of them and feeds back into your position sizing rules.

Risk: The Feedback Loop

Risk management isn’t a perfunctory phase to be tacked on at the end of the process. It's the thread that connects everything. Run precedent scenarios of all types so you can "shock your portfolio": if your top three positions break tomorrow, what happens to the book? What if China blocks all transactions involving US companies? What if tax inversion M&A deals have to be restructured or blocked via new regulations and no longer attractive to the buyers?

But risk management is also about recognizing when your process needs updating. Markets evolve. Regulatory attitudes shift, white papers are written by regulatory bodies and law firms. Financing standards change. The feedback loop forces you to cycle back through every phase: Does this deal belong in my universe? Should my filters be tighter? Has my ranking system caught this risk? Do I need to add anything new to our collective team diligence protocols?

I learned this during the Financial Crisis. Deals that looked bulletproof—solid buyers, minimal regulatory risk, tight financing—started breaking on systemic factors nobody had modeled. The process didn't fail, but it 100% taught me some lessons that guide me today. New filters for macro risk. New ranking factors for correlation. New scenario planning for tail events. These aren't wholistic changes, just new wrinkles and constraints inside my framework.

What's Actually Process

Some people dismiss information gathering altogether, but I think it's legitimate part of process for many risk arb managers, investors and traders. Flying to regulatory hearings, meeting management teams, staring down CFOs as if you're conducting interrogations—for some PMs, this creates a safety blanket of information that feels like real intel versus just reading merger agreements.

Going to a gaming license transfer hearing in Indiana because you're trying to understand regulatory risk. Whatever it takes to feel like you have a handle on the situation. Not everyone needs this embedded in their process, but this behavior can sometimes be the difference between relying purely on legal documents and having something that feels like actionable intelligence. Others need the fulcrum documents, 1-2 outside attorney's available and on retainer, and a good trader to find the forced seller blocks.

The key is whether these activities are systematic and repeatable, or just random relationship-building that makes people feel plugged in.

Process Compounds

Process doesn't just keep you alive. It compounds across cycles. The cleanest merger arb trades you make today may become distressed opportunities tomorrow. Clear Channel, TXU or United Rentals in 2008. Caesars through every lifecycle stage: merger arb, credit battle, post-reorganization equity, special situation activist equity. If you mapped the capital structure when you sized the equity arb, you could have participated—subject to mandate—in the roadmap when the cycle turned.

In the near future,

will be introducing, “Let’s Break a Deal.” We will strategically and tactically outline how live announced mergers transactions can break—not if they are going to break—so set those Twitter and Substack alerts.The Universal Application

Today’s discussion was centered around merger arb—the purest laboratory for me, for building systematic thinking. But these phases apply everywhere. Universe building. Filtering. Ranking. Diligencing. Sizing. Constructing. Managing risk. Whether you're picking stocks, evaluating job candidates, programming a strength training program, or even choosing where to live, the thinking system scales.

The beauty of merger arb as a teaching tool is the feedback loops stay tight. You know quickly when your process worked or failed. That discipline, that systematic approach to probability and risk—stays with you across various disciplines and endeavors.

Build the factory. Trust the process. Let it compound.

I’ll be writing more on governance, activism and investment process. I’ve lived and breathed these for years. I’ve also written about tokenization, Formula One, the NBA, and sometimes just tell a story worth remembering. Stay tuned.

You can also find me on Twitter at @MrMojoRisinX and @BeWaterltd.

Your Process Framework

(Adapt this. Make it yours.)

Universe Building: Track everything in your scope. Map the event paths. Update continuously.

Filtering: Hard rules first, soft judgment second. Make exclusions. Draw lines before you need them.

Ranking: Rank. Map. Context matters as much as math. Re-rank constantly.

Diligence: Read the fulcrum documents. Whiteboard failure modes. Build decision trees and probability weight different event paths before you trade.

Sizing: Rules-based with conditional triggers. Liquidity overlays. Hard caps on concentration. Don't break your sizing rules!

Trade Construction: Engineer positions based on deal structure. Hedge tail risks appropriately. Risk of Loss. Risk of Fraud.

Portfolio Construction: Know your risk. Stress-test worst cases. Plan your exits.

Risk Management: Continuous feedback loop. Scenario planning. Process evolution.

The phases cycle. The system evolves. The edge compounds.